Why settlement consulting is distinct from migration advice

Visa strategy determines lawful presence and work rights; settlement orientation addresses life administration after arrival. Conflating the two creates compliance risk for providers and confusion for families. We routinely refer migration matters to registered migration agents and focus our scope on post-arrival practicalities: how Medicare enrolment typically works for eligible visa holders, when to apply for a tax file number, how rental and utility arrangements interact with identity verification, and what financial product conversations should wait until you hold appropriate licences on the other side of the table.

Migrants who map systems early tend to make fewer costly mistakes — duplicating cover, signing product forms without reading disclosure, or handing banks incomplete KYC packs.

The first administrative sequence we commonly discuss

- Secure housing and identity documents — Confirm which identity documents Australian agencies and banks will accept from your visa class; plan certified copies where needed.

- Tax file number — Understand timing and online application pathways through the ATO; recognise that employers and banks may request TFN declarations even while applications are pending.

- Medicare eligibility — Clarify whether your visa subclass triggers enrolment, waiting periods or private health considerations; we explain concepts, not lodge clinical claims.

- Banking — Compare account types at a high level, noting that banks apply AML/KYC rules that can delay account opening if address or visa evidence is incomplete.

- Superannuation orientation — Explain default fund mechanics and when to seek licensed advice before consolidating overseas balances.

- Protection concepts — Introduce how life, health and general insurance differ in Australia and when a licensee must be engaged for personal recommendations.

Health and Medicare sequencing

Medicare eligibility depends on visa subclass. We clarify waiting periods and how private health cover may interact with your circumstances before you meet a licensee about hospital or extras products.

Household-specific topics

Families with school-age children

We outline how public and private schooling enrolment typically works at state level, what proof of address schools may request, and how this differs from jurisdictions where school place is tied to hukou or district registration. We do not guarantee placements; we reduce surprises in documentation timing.

Single professionals and couples

Focus often shifts to credit history absence, mobile phone contracts, and transport cards. We explain why a thin Australian credit file is normal and how licensed advisers may later assess borrowing differently from offshore records.

Later-stage arrivals joining employed sponsors

Dependency on a sponsor’s existing accounts can obscure individual TFN and Medicare steps for secondary applicants. We map separate obligations so secondary applicants are not administratively invisible.

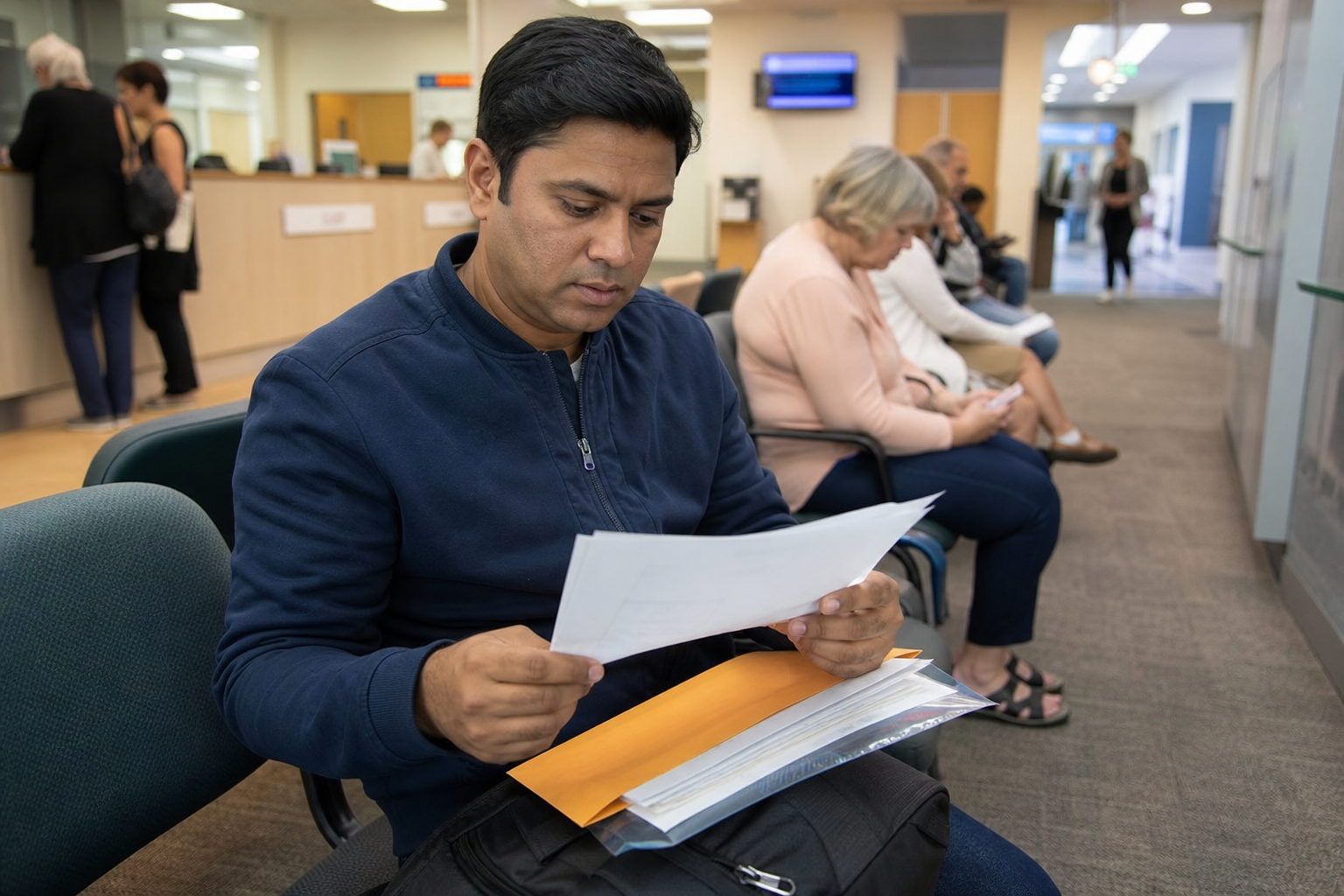

Banking and early appointments

Banks apply AML/KYC rules that can delay account opening when address or visa evidence is incomplete. We help you sequence TFN, Medicare and banking appointments so you are not repeating the same paperwork three times in one week.

Settlement support should not rush product sales. Under relocation stress, families are vulnerable to unsuitable products if disclosures are skipped. We record when a referral to an AFSL licensee is appropriate and obtain consent before introductions.

Financial product boundaries during settlement

It is common for newcomers to be offered bundled “new arrival” packages. We teach clients to ask: Is this factual information, general advice or personal advice? Who holds the AFSL? Where is the PDS? If answers are unclear, pause and seek a licensee you choose independently — including one we introduce with documented handover.

We do not recommend specific insurers, funds or lenders. We explain categories — for example, private health hospital cover versus extras, or life insurance through super — so your licensee meeting addresses your circumstances rather than glossary basics.

Working with other professionals

Settlement runs parallel to tax residency questions, property purchases and business setup. We coordinate timelines with your accountant and lawyer where you authorise communication, so TFN, entity registration and personal protection discussions align rather than conflict.

Centrelink and concession cards

Eligibility for certain payments and cards depends on visa subclass and residency tests. We explain where to find official information and when Centrelink enquiries should be self-directed — we do not lodge Centrelink claims.

Engagement options and fees

Consulting may be a single briefing, a structured multi-session programme, or ongoing check-ins during your first year. Fees depend on scope and household complexity; we confirm in writing before work begins. Request a quote with your visa subclass (general terms only), arrival date and family composition for a scoped proposal.

Related services: Compliance Readiness, Market Orientation, Referral Process. Read our insight on the first 90 days or view a case study.