Weeks 1–2: foundation without product noise

Priority is stable address evidence, emergency contacts, and school enquiries if children are school-age. We discourage binding financial product commitments in week one — travel cover marketed as permanent health cover is a recurring mistake. Certified copy requirements for later bank visits should be identified early using each agency’s published rules.

Weeks 3–5: identifiers and health system access

Tax file number applications for adults should be planned before employer payroll deadlines. Medicare eligibility depends on visa subclass — we explain waiting periods and private health interactions without recommending specific funds. Secondary applicants on family visas need their own administrative steps; relying solely on the primary applicant’s accounts creates gaps.

Planning the first quarter

Households that map TFN, Medicare and banking in sequence avoid repeating the same documents at three counters in one week. The calendar is adjusted for visa class and dependants.

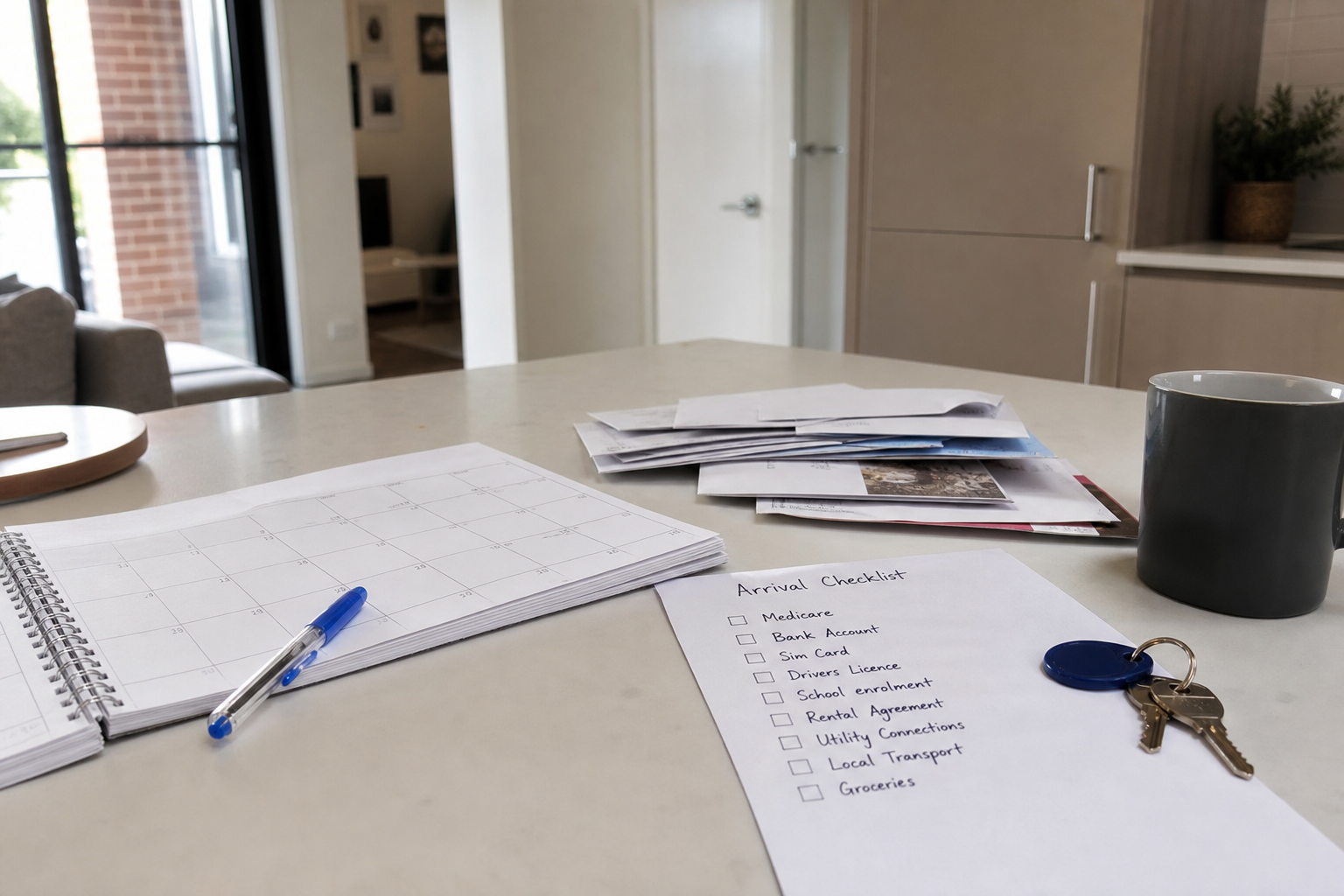

Weeks 6–8: banking with a complete pack

Bank deferrals in this period usually trace to address mismatch or missing visa evidence, not “bias” against newcomers. A structured second appointment with a pre-verified pack outperforms repeated walk-ins. We do not recommend institutions; we align documents to the institution you choose.

Weeks 9–12: orientation before licensee meetings

Super default fund mechanics and insurance categories should be understood before RFPs to advisers. Our market orientation fills this gap. Referral to an AFSL licensee follows only with documented consent if personal advice is needed.

“Do everything in week one” social media advice often creates parallel errors — duplicate policies, wrong Medicare assumptions, and TFN stress with employers. Sequencing is cheaper than unwinding.

When to accelerate or pause

Skilled migrants with immediate employment may compress TFN and banking. Student or provisional pathways may require different health cover understanding. Business owners arriving on investor or business visas need parallel entity conversations — see cross-border consulting rather than forcing personal settlement templates onto corporate matters.

Full service: New Migrant Settlement · Case study: Migrant family banking