Problem

The family’s prior migration agent had focused on visa grant only. They attended a major bank branch with overseas passports and visa grant letters but without Australian residential address proof acceptable under that bank’s policy. Accounts were deferred twice. Meanwhile, the primary applicant’s employer requested TFN details within 14 days. Secondary applicant had not applied for Medicare despite eligible subclass. Stress and conflicting advice from social media forums compounded poor decisions — including nearly purchasing travel insurance marketed as “health cover” for permanent residents.

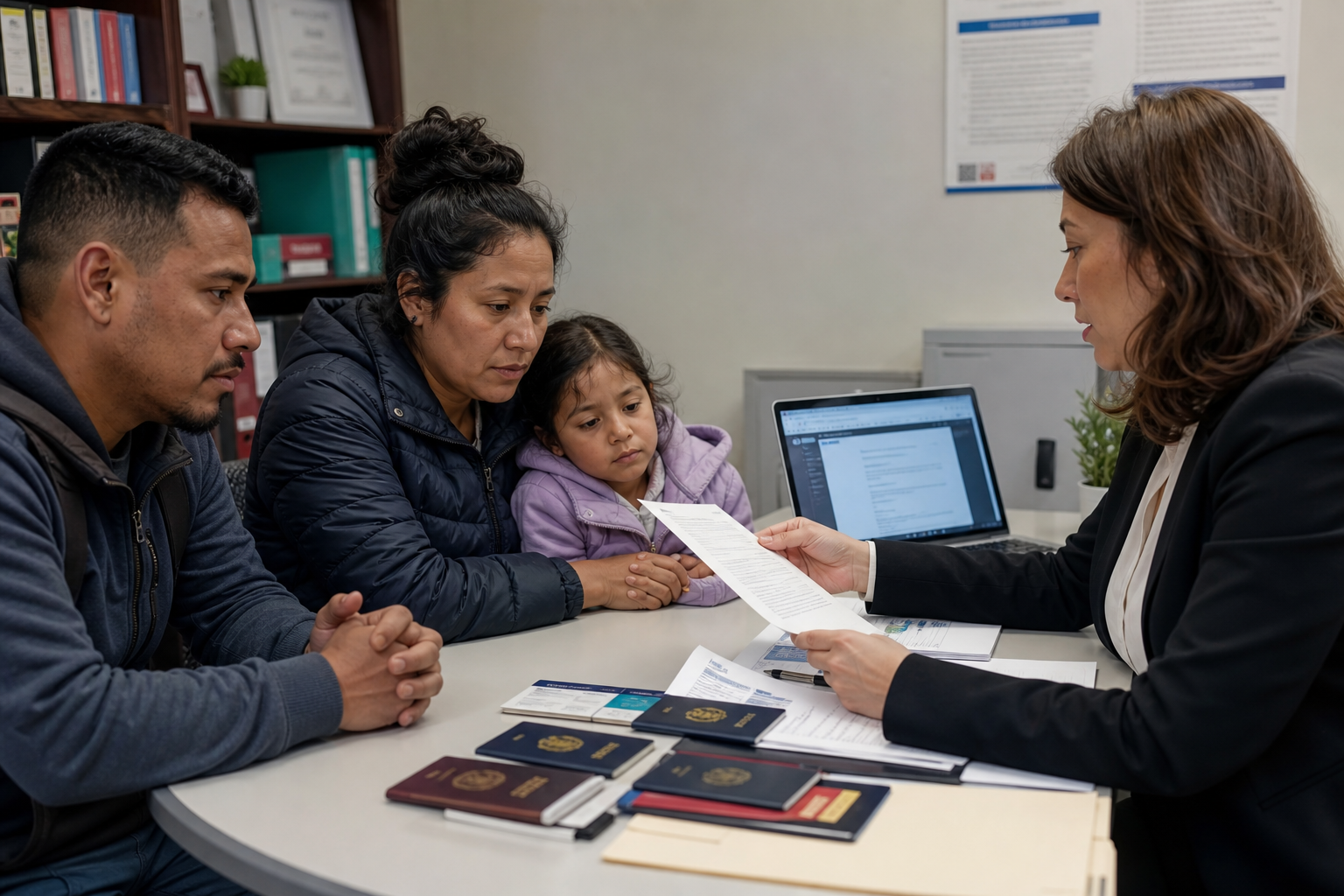

Our approach

- Mapped a corrected sequence: address evidence → TFN online applications for adults → Medicare enrolment where eligible → bank appointment with pre-verified document pack.

- Prepared a one-page employer letter template for TFN pending status (information only; client’s HR approved use).

- Explained difference between visitors cover, OVHC (where relevant) and Medicare — without recommending products.

- Identified that super default fund choice could wait until after TFN stabilisation; scheduled market orientation before any consolidation discussion.

Measures implemented

- Certified copy guide aligned to each agency’s published requirements

- Shared calendar with milestones and responsible family member per task

- Single point of contact at Wealth Insurance for questions to avoid contradictory WhatsApp advice

Outcome

Bank accounts opened on second structured visit (week 3). TFNs issued for adults by week 2. Medicare cards requested with correct waiting period understanding. Employer payroll issue resolved without penalty. Family declined immediate product sales call from a non-licensee marketer; later chose to accept our referral to an AFSL licensee for life cover review after orientation briefing.

Client-reported result: “Administrative chaos reduced; we knew which professional to use for each next step.”

Lessons for similar households

Arriving with a pre-booked bank appointment is only efficient when TFN and address evidence align with that bank’s policy. Social media “shortcuts” frequently omit visa-specific Medicare rules. Families should assign one member to own each agency relationship to avoid contradictory submissions. Product marketers targeting new estates are common; pausing until after orientation reduced unsuitable cover purchases in this case.

Metrics

Four consulting sessions delivered over four weeks; two licensee meetings avoided in week one due to incomplete packs; one successful referral after orientation with documented consent. No complaints lodged; client feedback collected verbally and noted in file.

Professional measures that differentiated this engagement

We issued a written scope limiting services to settlement and readiness — explicitly excluding migration advice. Each session ended with a one-page action list assigned to named family members. We declined a request to “call the bank manager” to expedite approval, explaining that relationship pressure does not replace KYC rules. When a travel insurer marketed hospital cover as equivalent to Medicare, we documented the distinction in writing for the family file.