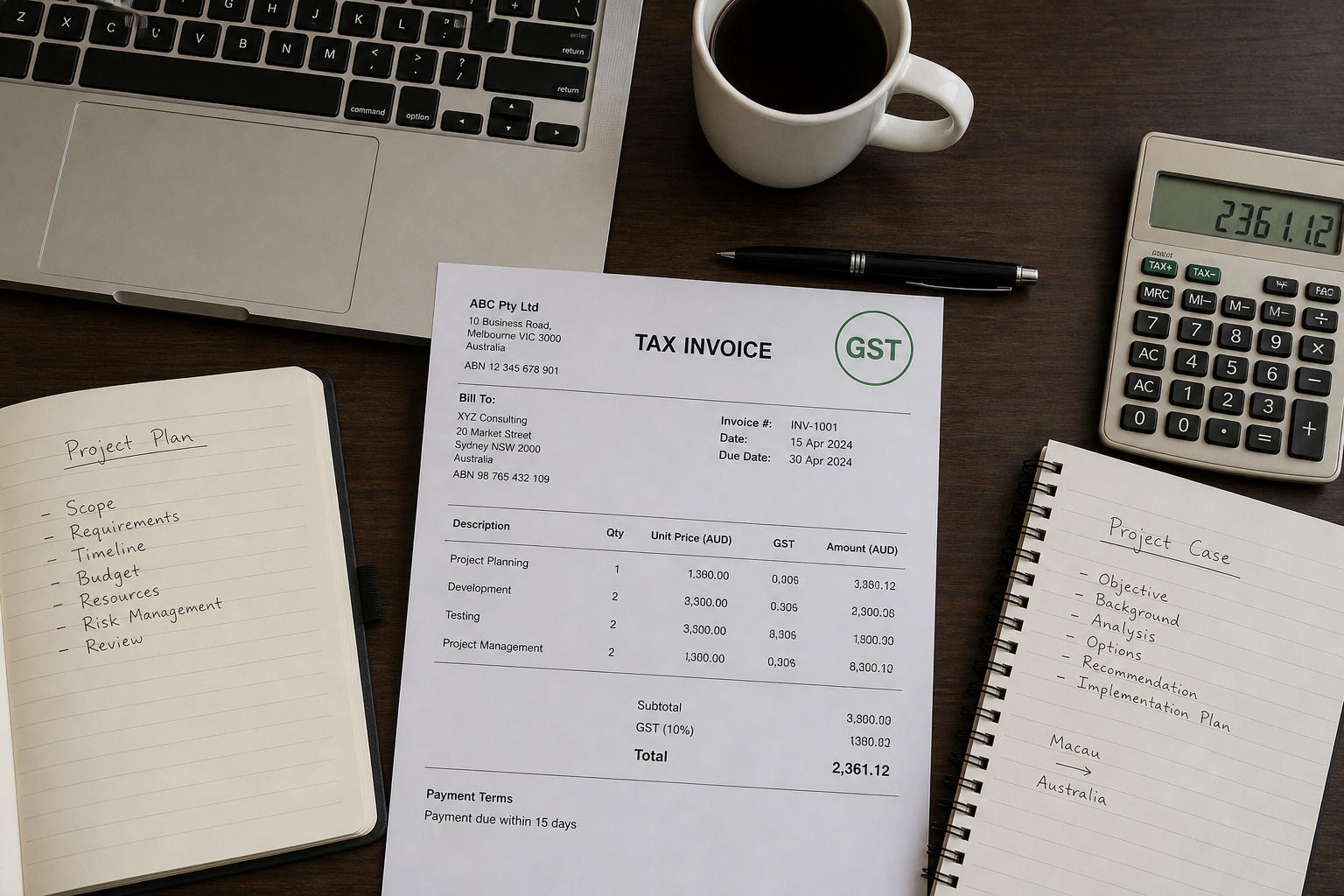

Problem

Australian customers requested tax invoices with ABN. Macau firm had no Australian entity and applied Macau invoice formats. Customers withheld 10% citing confusion; firm feared double taxation. Director considered rushing Australian company registration solely for invoicing without understanding GST registration thresholds or permanent establishment concepts at a high level.

Our approach

- Orientation on when Australian registration is necessary versus agent or branch alternatives (legal/tax detail referred to practitioners).

- Explanation of GST registration triggers and BAS obligations at overview level.

- Facilitated introduction to registered tax agent with cross-border experience (client choice).

- Invoice template checklist — what Australian B2B customers typically require (ABN, GST line items where applicable).

Measures implemented

- Paused incorrect ABN applications attempted with wrong entity type

- Tax agent engaged week 2

- GST registration timing aligned with projected Australian turnover

Outcome

Valid Australian invoicing structure implemented by tax agent; customer withholdings resolved. Macau firm did not open unnecessary shelf company. Director reported clearer understanding of when to escalate to lawyer for permanent establishment analysis before scaling headcount in Australia.

Difficulties encountered

Macau accounting staff used Portuguese invoice templates incompatible with Australian GST line requirements. Australian customers applied incorrect withholding pending ABN clarity. Director nearly registered a dormant Australian company with wrong activity codes.

Resolution techniques

We paused registrations, convened tax agent within one week, and issued bilingual glossary of terms (GST, BAS, ABN) for Macau finance team. Invoice template approved by tax agent before resuming billing.

Outcome validated by tax agent sign-off on first compliant invoice cycle; no regulator contact. Client continued consulting for potential Australian subsidiary in year two — separate scope.